Most IDFC FIRST borrowers know their EMI amount but not where it goes, what missing one payment triggers, or why the credit card minimum due is a trap. Here is all of it in plain language.

Getting a loan approved feels like the hard part. The paperwork, the documents, the waiting. Once the money lands in the account, most borrowers stop paying close attention. That is exactly when they should be paying the closest attention.

The repayment side of an IDFC loan repayment is where the real cost of borrowing lives. This article covers what most borrowers only discover when something goes wrong.

For IDFC FIRST borrowers settling their monthly EMI or credit card bill, Bajaj Pay, the BBPS payments platform on Bajaj Finance, shows the exact amount due before you confirm and completes the payment in under two minutes through UPI, cards, or net banking.

The Thing About Your EMI That Most People Never Notice

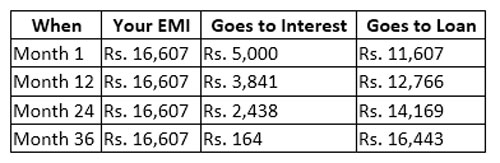

Every month, your IDFC loan repayment goes to two things: the interest on what you owe, and the actual loan amount you are paying back. The split is not equal, and it changes over time.

In the early months, most of your EMI is going toward interest. Not toward actually reducing the loan.

Here is what that looks like on a typical Rs. 5 lakh personal loan. Numbers are illustrative.

Same EMI every month. But in month one, nearly a third of it is interest. By the last month, almost all of it reduces the loan itself.

Why does this matter? Because if you ever want to pay extra toward your loan, the earlier you do it the better. An extra payment in the first year saves you far more than the same payment in the third year. The loan is at its heaviest at the start. That is when extra payments hit hardest.

What Happens When You Miss a Payment

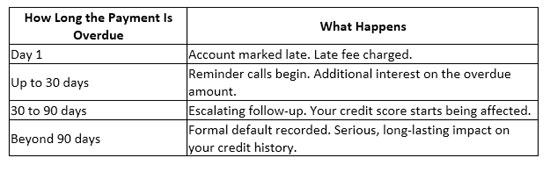

Most people assume missing one EMI means a reminder call and a small fine. The reality moves faster than that.

The bank marks your account as late on the same day the payment was due, per RBI guidelines. A late fee applies that day. After that, the longer the payment stays unpaid, the more serious it gets.

Here is the part most borrowers do not know at all.

If one loan goes past 90 days without payment, every loan you have with the same bank is affected, per RBI guidelines. Not just the one you missed. Your personal loan, your home loan, your credit card, all of them.

One overdue payment does not stay in one place. It spreads across your entire relationship with the bank.

The Credit Card Minimum Due Is Not What It Looks Like

Your IDFC FIRST credit card statement every month gives you two numbers. The total amount you owe. And the minimum due, which is a much smaller number.

Paying the minimum due means your account is not in default. That is the only good thing about it.

The day after your due date, interest starts on everything you did not pay. Not just the amount above the minimum. On the entire outstanding balance.

An IDFC credit card payment of the full amount before the due date costs you nothing extra. Paying only the minimum due means interest starts running on the rest immediately, at one of the highest rates in personal finance.

A few months of minimum due payments can turn a manageable balance into a difficult one. The minimum due is for genuine emergencies. It is not a habit.

Three Simple Things That Prevent Most of This

- Set up auto-debit from day one. Ask IDFC FIRST to link your EMI to your bank account so the amount is deducted automatically every month. No reminder needed. No action from you. If auto-debit is not already running on your loan, call the bank and set it up.

- Pay your credit card in full every month. If a particular month is tight, pay as much above the minimum as you can. Every rupee above the minimum reduces what interest applies to.

- Pay a day or two before the due date, not on it. Payments can take a day to process. A payment made on the due date sometimes arrives the next day. The bank marks accounts late from the due date itself, not from when you pressed pay.

Pay Your IDFC FIRST Loan or Credit Card Bill on Bajaj Finance

Your EMI and credit card due dates fall on fixed dates each month. Paying before them costs nothing. Bajaj Finance processes both IDFC FIRST loan payments and credit card payments through BBPS with instant confirmation.

Steps to pay your IDFC FIRST loan EMI or credit card bill:

- Open the Bajaj Finance app or visit bajajfinserv.in and log in

- Go to Bills and Recharges and select Loan Repayment or Credit Card Payment

- Select IDFC FIRST Bank and enter your loan account number or credit card number

- Review the exact amount due before confirming

- Choose a payment method and save the instant confirmation receipt

A loan is not over when it is approved. It is over when the last EMI clears. Pay before the due date. Pay your credit card in full. Set up auto-debit once so you never have to think about it again. The consequences of getting this wrong are not small and they move quickly.