Buying a term insurance policy is one of the most important financial decisions a person makes. It is meant to protect the family when the earning member is no longer around.

But many people make mistakes while choosing one. These mistakes seem small at the time. Later, they can cost the family a great deal.

Here are the most common ones to watch out for.

Thinking 2 Crore Is Always Enough

Many buyers pick a 2 crore term insurance cover because it sounds like a large number. But they never calculate if it is actually enough.

A simple way to estimate the right cover is to multiply yearly income by fifteen and add any outstanding loans on top. That gives a more realistic number than guessing.

Choosing the Cheapest Plan Without Checking the Insurer

The cheapest 2 crore term insurance plan is not always the best one. A low premium from an unreliable insurer is a risk, not a bargain.

Before deciding on price, check two numbers from the IRDAI annual report. The claim settlement ratio shows how many claims were paid. The amount settlement ratio shows whether large claims like a 2 crore payout were also settled. Both matter. A company can show a high claim count while quietly rejecting big payouts.

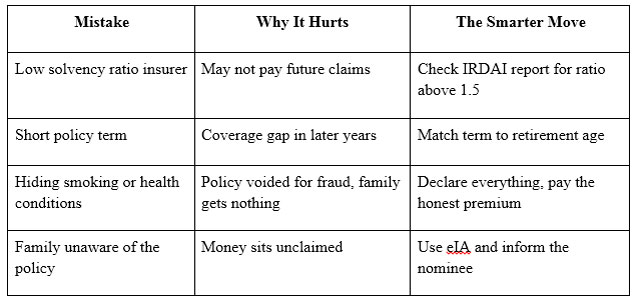

Not Checking the Solvency Ratio

The solvency ratio shows if an insurer has enough money to pay future claims. IRDAI requires a minimum of 1.5. A company at 2 or above is on stronger ground. This number is publicly available and takes minutes to check.

Picking the Wrong Policy Term

A 35 year old who buys a 20 year plan has no coverage from age 55 onwards. If the plan is to work until 65, that is a ten year gap with nothing in place.

Match the policy term to the retirement age. Some plans offer coverage up to 75 or 80. The slightly higher premium is worth the complete protection. A term insurance policy should cover the working years, not just a part of them.

Ignoring the Increasing Cover Option

Two crore rupees today will not carry the same value twenty years from now. Some plans offer an increasing cover option where the sum assured grows by 5 to 10 percent every year. This keeps the cover relevant as costs rise over time.

Hiding Health Information at the Time of Application

This is the most damaging mistake of all.

Insurers ask about existing illnesses, smoking habits, alcohol use, and family medical history. Some buyers hide this to get a lower premium. If this comes to light during a claim, the claim gets rejected.

But it goes further than rejection. If a smoker applies as a non-smoker and the insurer discovers this at the time of a claim, the entire policy can be declared void for fraud. The family receives nothing. Not a reduced amount. Nothing.

Under Section 45 of the Insurance Act, an insurer cannot question a policy after three years of it being active. But that protection only applies to honest policies. A fraudulent application does not get that benefit.

Full disclosure from day one is the only safe approach.

Delaying the Purchase

A 28 year old with clean medical reports pays far less than a 45 year old with high blood pressure or early diabetes. For a 2 crore cover, most insurers require a full medical check-up. Waiting increases the chances of a loaded premium or even a rejected application. Buying early avoids all of this.

Not Telling the Family About the Policy

Many families never claim because they did not know a policy existed. Opening an e-Insurance Account, also called eIA, solves this. It works like a Demat account but for insurance policies. All policies sit in one digital place. The nominee can find everything easily without searching through paperwork.

Always share the eIA login or a physical copy of the policy with the nominee.

Quick Reference - Mistakes and Fixes

Checklist Before Buying a 2 Crore Term Insurance Policy

- Calculate: Yearly income multiplied by 15, plus all outstanding debts

- Verify: Check the latest IRDAI annual report for claim and benefit amount settlement ratios

- Digitise: Open an e-Insurance Account to store the policy digitally

- Disclose: Declare all habits and existing conditions honestly, including minor ones like thyroid or blood pressure

- Inform: Give the nominee the eIA login or a physical copy of the policy document

Buying a 2 crore term insurance policy the right way does not take long. But the decisions made at the time of purchase determine whether the family is truly protected or left struggling when it matters most.